Comparing the paid-up additional insurance dividend option with the enhanced insurance dividend option

We offer 5 dividend options on Sun Par Protector II and Sun Par Accumulator II policies:

- paid-up additional insurance (PUA)

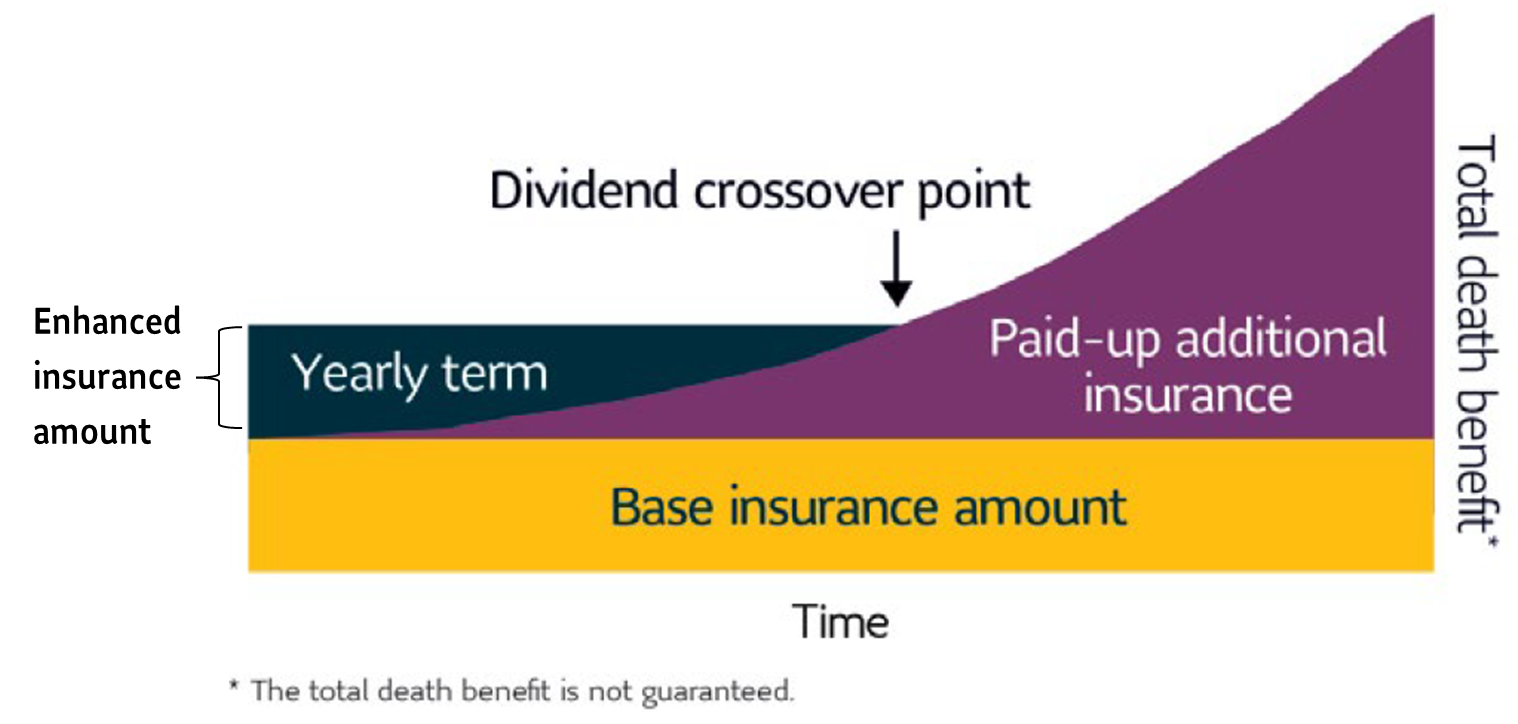

- enhanced insurance (ENH)

- annual premium reduction

- dividends on deposit (DOD)

- cash payment

Regardless of the dividend option selected, all our par policies share the same guarantees:

- guaranteed initial face amount

- guaranteed base premiums

- guaranteed cash values

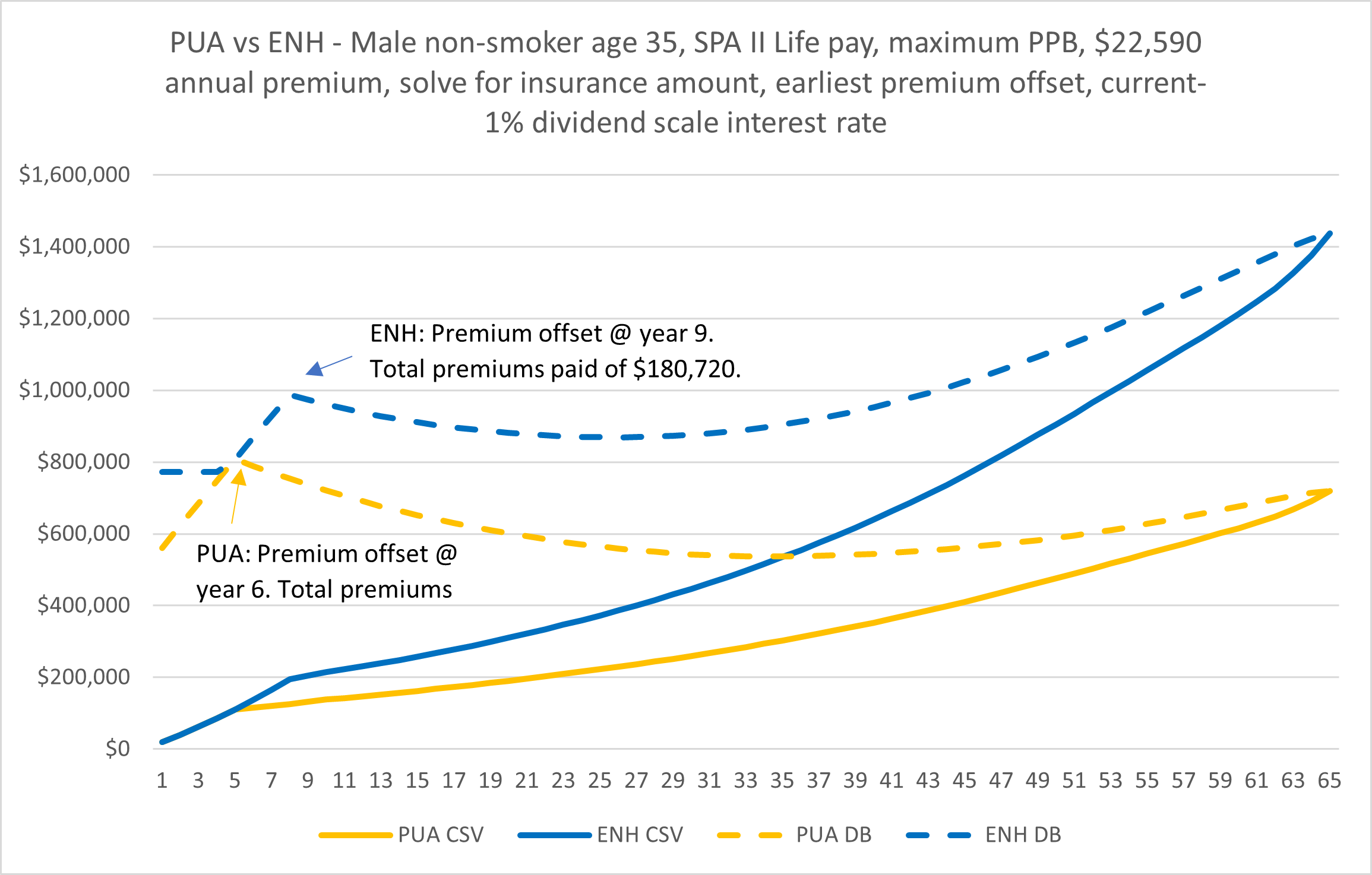

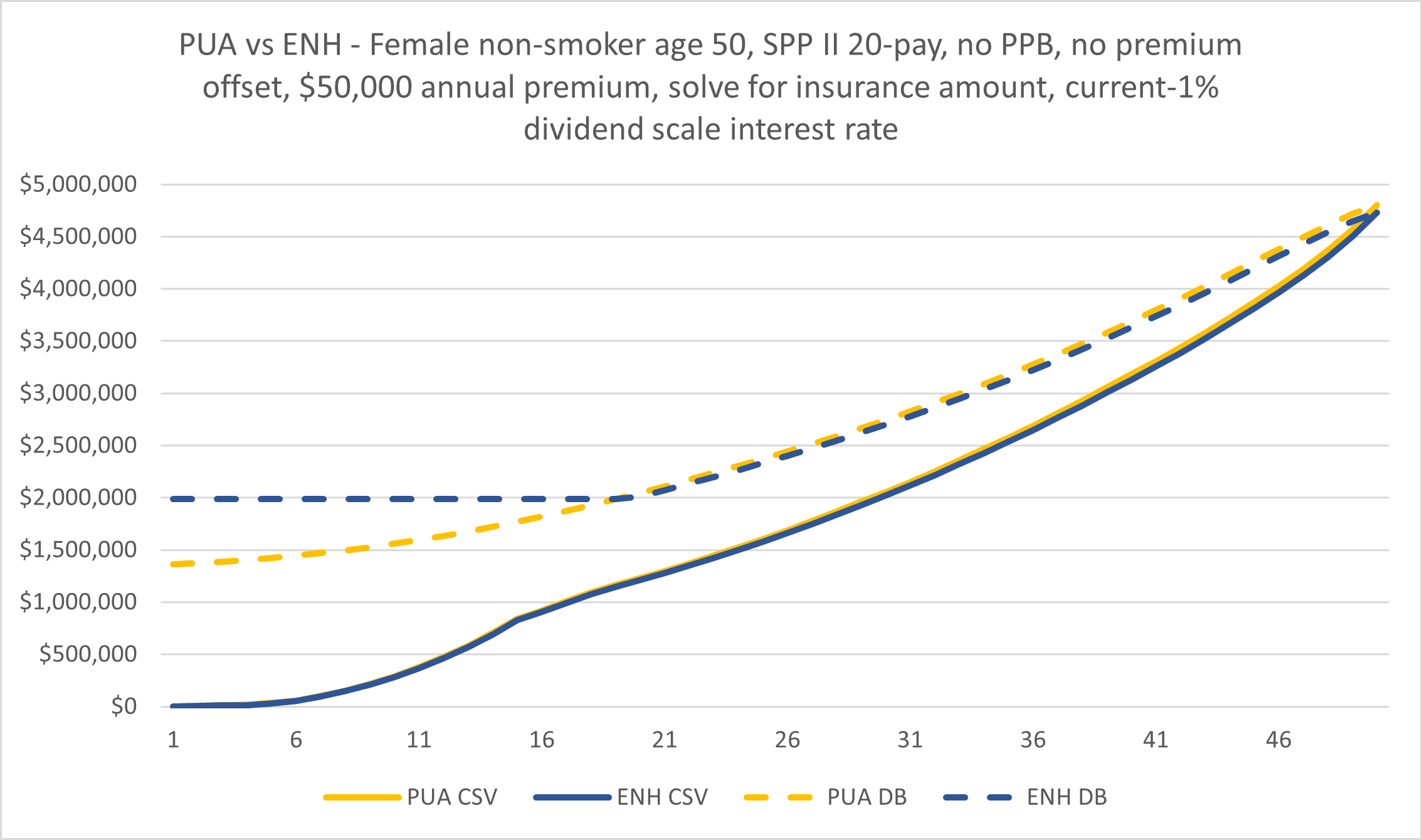

The most popular dividend option is PUA. However, for certain Clients selecting the PUA dividend option, the ENH dividend option may be the better choice. So how would you know when to recommend the PUA dividend option or the ENH dividend option?

First, let’s look at these two different dividend options and how they work…

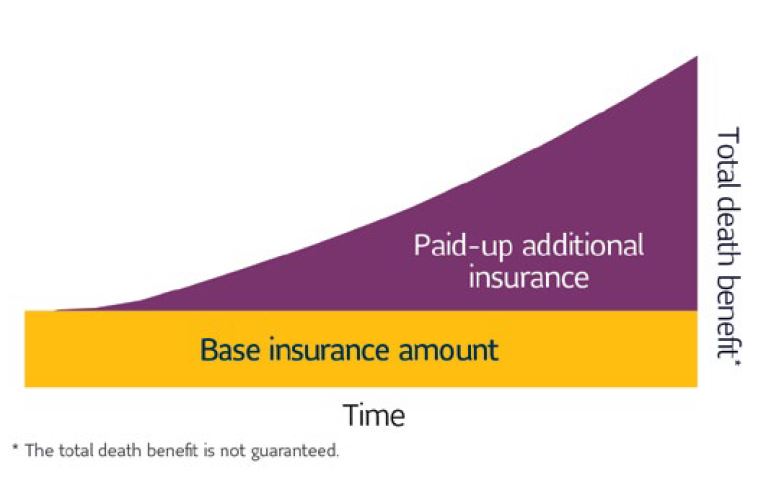

Paid-up additional insurance (PUA) dividend option: