The Capital Dividend Account (CDA)5 is part of the system of integration in the Income Tax Act (ITA)6.

One of the key advantages of corporate ownership of life insurance is the ability for the shareholders to receive tax-free dividends through the CDA, as stated in paragraph (d) of the definition of "capital dividend account" in subsection 89(1) ITA. Under this provision the net proceeds of a life insurance policy will be added to the CDA of a private corporation.

The expression "net proceeds" is defined as the amount of the life insurance policy proceeds received as a consequence of the death of the person insured minus the adjusted cost basis (ACB) of the policy immediately before the death of the person insured.

Example:

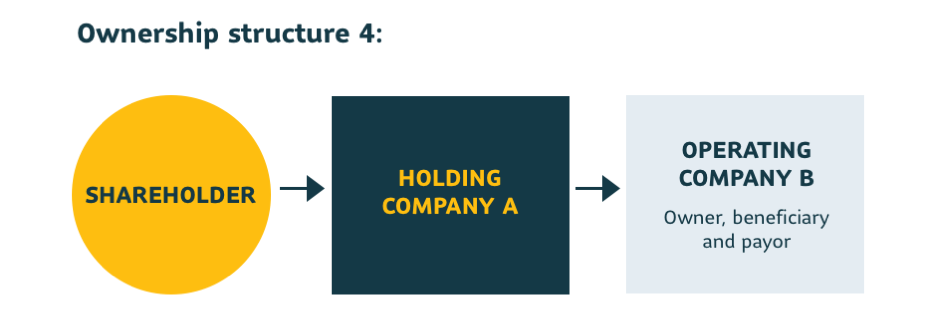

A private corporation7 is the beneficiary of a life insurance policy with a death benefit of $1,000,000.00. The ACB of the policy at the time of the insured shareholder's death is $150,000. The amount that will be credited to the corporation's CDA is $850,000 ($1,000,000 - $150,000). This amount can be paid tax-free to the shareholders of the corporation as a capital dividend. The balance of $150,000 can be paid to the shareholders as a taxable dividend.

Multiple corporations and the CDA

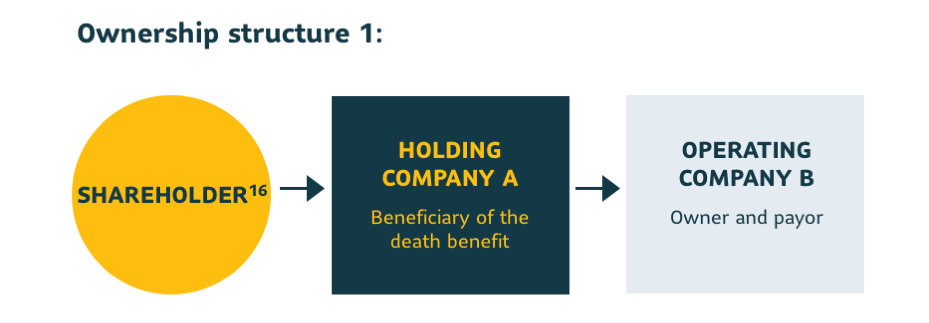

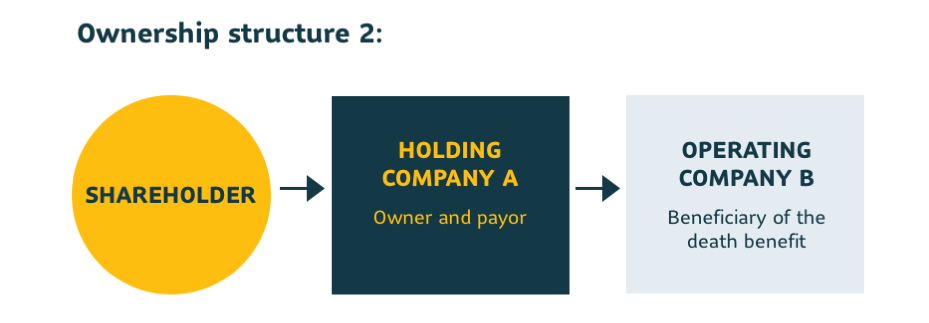

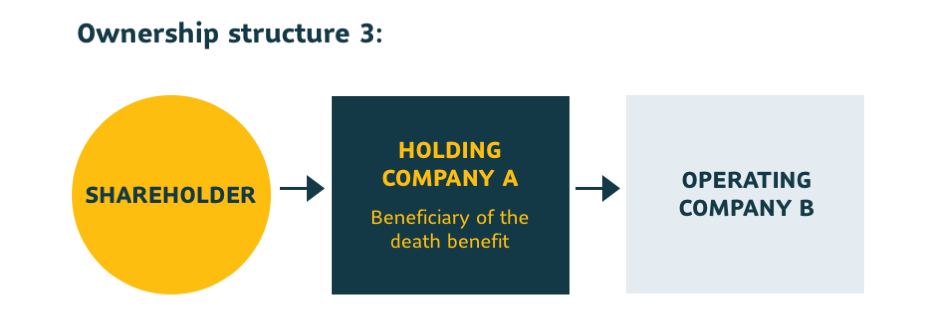

The Canada Revenue Agency (CRA) has consistently taken a position against arrangements designed to unduly exploit the preferential treatment accorded to the CDA where a corporation receives life insurance proceeds8. Certain life insurance ownership structures previously allowed corporations to receive the full death benefit as a credit to their CDA, without a corresponding reduction for the policy's ACB.

This was often accomplished by having a holding company own the policy, but then designating an operating company as the beneficiary of the life insurance proceeds. Because the operating company did not own the policy, it could claim the full death benefit as a CDA credit without a reduction for the ACB of the policy.

The 2016 federal budget ended this practice for deaths occurring on or after March 22, 2016. As a result, the death benefit is now reduced by the ACB for purposes of calculating the CDA credit, regardless of the structure in place for corporate ownership of the life insurance policy.

The 2016 federal budget also proposed the introduction of an information-reporting mechanism that will apply where a corporation or partnership is not a policyholder but is entitled to receive a benefit under the policy. Over the years, the CRA has often expressed opposition to two separate corporations being designated as policyholder and beneficiary solely to benefit from the CDA. The new reporting requirement will enable the CRA to detect this type of situation at the outset, without having to wait until the CDA is calculated at the time of the insured person’s death.

Creditor protection for the policy

Subject to the exceptions provided for in the Bankruptcy and Insolvency Act and provincial Insurance Acts9, a life insurance policy that has a cash surrender value constitutes an asset that can generally be seized by the policy owner's creditors. For example, a policy owned by a corporation will form part of the corporation's assets and the cash surrender value of the policy could be seized by the trustee in the event of bankruptcy. Furthermore, if the insurance was purchased to fund a shareholders' agreement, the death benefit payable to the corporation on the death of one of the shareholders could be subject to the claims of the corporation's creditors. Certain corporate ownership structures can be put in place to guard against this risk.

Where a corporation is the owner of a life insurance policy, the policy is protected from the shareholders' personal creditors or from legal proceedings against one of the shareholders10. The insurance policy could also be owned by a holding company that is, in turn, a shareholder of an operating company. Under this policy ownership structure, it is possible for the policy to be protected against the creditors of the operating company, as long as the holding company is not the guarantor of any of the operating company's obligations. The segregated funds in a registered products like RRSP, RRIF provided NO protection against familial patrimony rules, if applicable. Finally, the segregated funds could be in the partition process in a divorce according to the matrimonial regime.

It must be kept in mind that this protection is not total, and it does not apply in all situations. For example, transferring funds into a life insurance policy or choosing a particular corporate ownership structure for a policy does not confer absolute protection against creditors, nor does it automatically make the policy exempt from seizure if the trustee is able to prove that the purpose of the transaction was to defeat the claims of creditors.11

When in doubt as to the legal risks relating to corporate ownership of life insurance, consult a legal advisor.

5 Subsection 89(1) of the Income Tax Act (ITA) defines various types of property and distributions including the contents of the Capital Dividend Account. In Quebec, paragraph b of section 570 of the Taxation Act (TA) refers to the ITA. CRA Interpretation Bulletin IT-66R6 reviews the inclusions in the CDA and the CDA mechanism.

6 Refer to the Capital Dividend Account tax guide published by Sun Life Financial for more information on this topic at: the-capital-dividend-account-en.pdf

7 CDA is not available for public corporations.

8 In particular by applying the General Anti-Avoidance Rule (GAAR). See CRA Technical Interpretation 2004-0065461C6, CRA Income Tax - Technical News No. 44 dated April 14, 2011, and CRA Technical Interpretation 2010-0371901C6.

9 Refer to the Bankruptcy and Insolvency Act, R.S.C. 1985, c. B-3 (BIA). In Quebec, the relationship between the owner and the beneficiary determines whether or not the policy is protected; see articles 2455, 2456, 2457 and 2458 of the Civil Code of Quebec (CCQ).

10 Subject to the lifting of the corporate veil and any personal guarantees given by the shareholders to the creditor, if applicable.

11 See the decision of the Supreme Court of Canada in Royal Bank of Canada v. North American Life Assurance Company and Balvir Singh Ramgotra, [1996] 1 SCR 325.