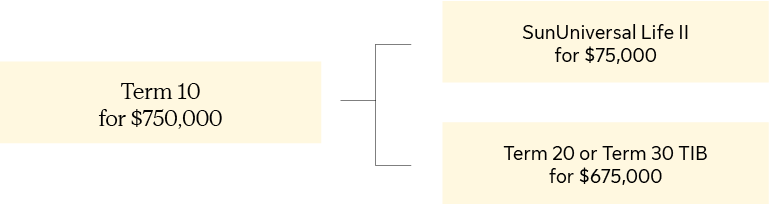

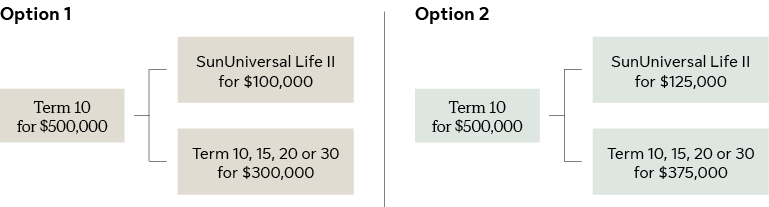

When Clients convert their term policies, they often don’t convert the full face amount to permanent insurance. But they may still need temporary insurance. Now, it’s easier for Clients to keep more of their coverage when converting term insurance.

In many cases, Clients who partially convert their eligible term policy to permanent insurance can carry over some, or all, of the remaining term coverage without underwriting. The remaining term coverage becomes a new term insurance benefit (TIB) on their new permanent policy.