- Search

- Search

-

New business and underwriting

Competitive edge: Fixed income quality and duration

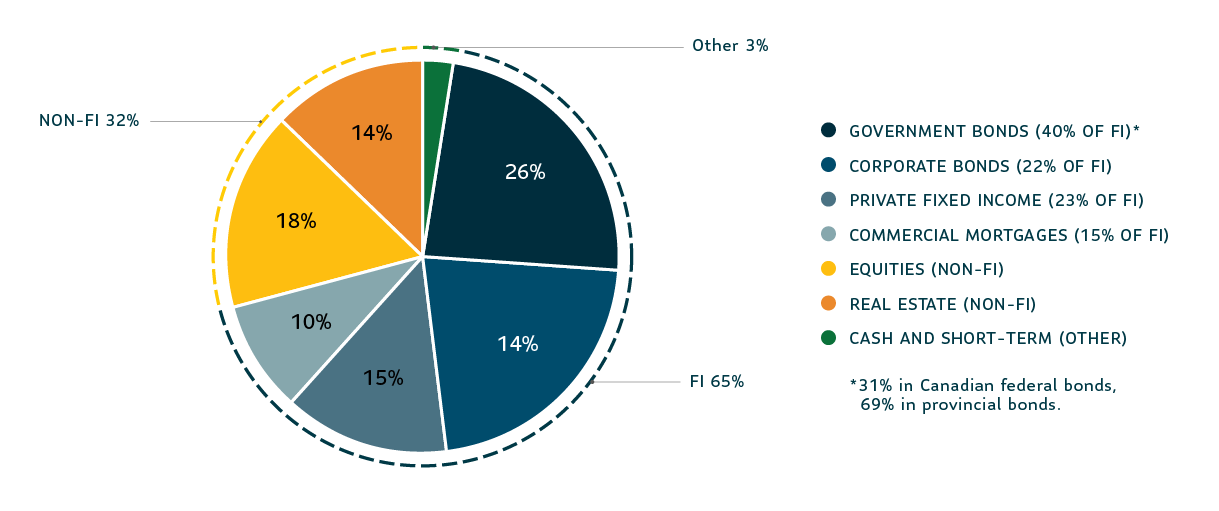

Par Fixed Income

All values as of December 31, 2021

Fixed income assets are an important part of any portfolio, offering stability as well as growth. That’s why any Canadian insurer’s Par account is typically made of up to 60%-80% fixed income assets, such as bonds, mortgages and private fixed income. However, not all fixed income assets are the same. The type, quality and duration can play a big role in overall portfolio growth. Below we’ll look some of the ways in which Sun Life approaches this aspect of portfolio management.

Well-diversified by asset mix

Sun Life’s asset mix doesn’t change much from year to year. However, we actively manage it by seeking opportunities to add incremental yield by trading between assets and quality. Other insurance companies may have reallocated their maturing fixed income assets and new premiums into more volatile alternative investments or lower quality fixed income to chase higher yields.

*31% in Canadian federal bonds, 69% in provincial bonds.

Balancing exposure across durations

We don’t bet on the direction of interest rates. Instead, we focus on purchasing appropriate high-value assets to match the long-term nature of our liabilities (death claims).

| Years to maturity |

0 to 5 years |

5 to 10 years |

10 to 15 years |

15 to 20 years |

20+ years |

Total |

|---|---|---|---|---|---|---|

| Public bonds |

10.4% |

18.4% |

14.4% |

21.3% |

35.5% |

100% |

| Private fixed income |

16.7% |

34.4% |

16.7% |

14.0% |

18.2% |

100% |

| Mortgages | 25.0% | 48.9% | 18.1% | 5.9% | 2.2% | 100% |

| Total fixed income |

14.1% |

26.8% |

15.5% |

17.2% |

26.4% |

100% |

Interest rates may be on the rise, but they remain low in comparison to what we experienced decades ago. Maturing bonds will likely rollover into lower yields. Sun Life has the lowest percentage of fixed income maturing in the next five years (14.1% as of December 31, 2021). In comparison, our major Par competitors have 25-50%. And the quantity of our new premiums relative to our Par account size is only 3-5%. As a result, the current low interest rate environment should have less impact to our portfolio. In contrast, when interest rates increase, there is a lagged impact to an insurer’s Par dividend rate. However, those who have a greater percentage maturing in the short term may see their portfolio yield increase sooner and more rapidly.

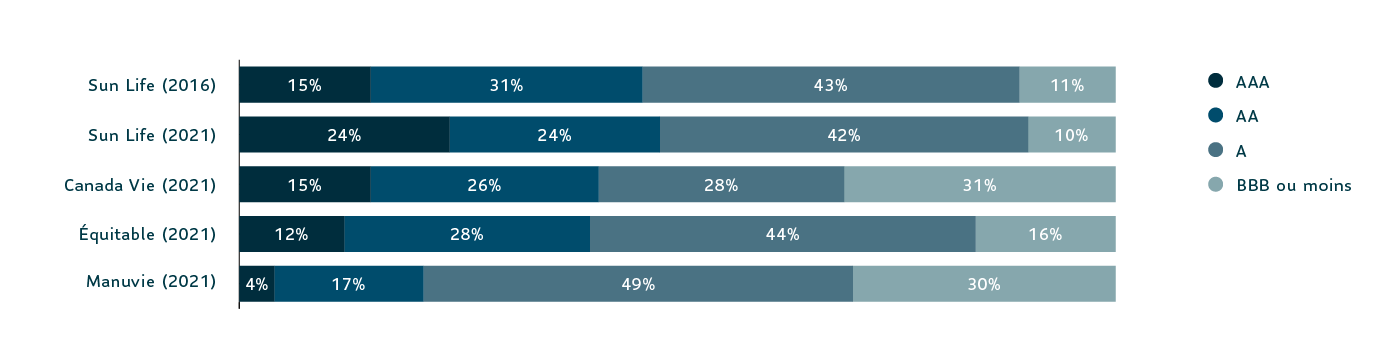

Well-diversified by asset quality

Rating agencies group bonds into categories based on their expected level of default risk. But the spread (difference in annual yields) between grade categories may change. When spreads compress, seeking additional return may come at the cost of a disproportionate increase in risk. While spreads declined in recent years, Sun Life shifted its bond portfolio up in quality. Over the same time, some other insurers shifted down in quality, opting for slightly more yield in this narrower spread environment.

Spreads have been low over the last few years but are now starting to widen. Sun Life may shift some liquid assets opportunistically toward lower grade bonds to capitalize on the improved risk-adjusted returns.

Sun Life’s prudent fixed income investment philosophy

We have a lower proportion of assets maturing in the current low interest rate environment as compared to other insurers. We believe lower-quality bonds have been inadequately compensated for their increased risk because of recent spread compression. As such, our significant percentage of high-quality bonds has positioned us well. We foresee a widening of spreads in the future. The increased liquidity of our high-quality assets puts us in a strong position to jump on opportunities. We actively manage our Par account to seek quality investments while staying within our target guidelines.